Are you struggling with inaccurate information on your credit report? You're not alone. Millions of Americans face the same challenge every year. The good news is that federal law, specifically Section 609 of the Fair Credit Reporting Act (FCRA), gives you powerful tools to dispute errors and potentially remove inaccurate items from your credit report.

What Is a 609 Dispute Letter?

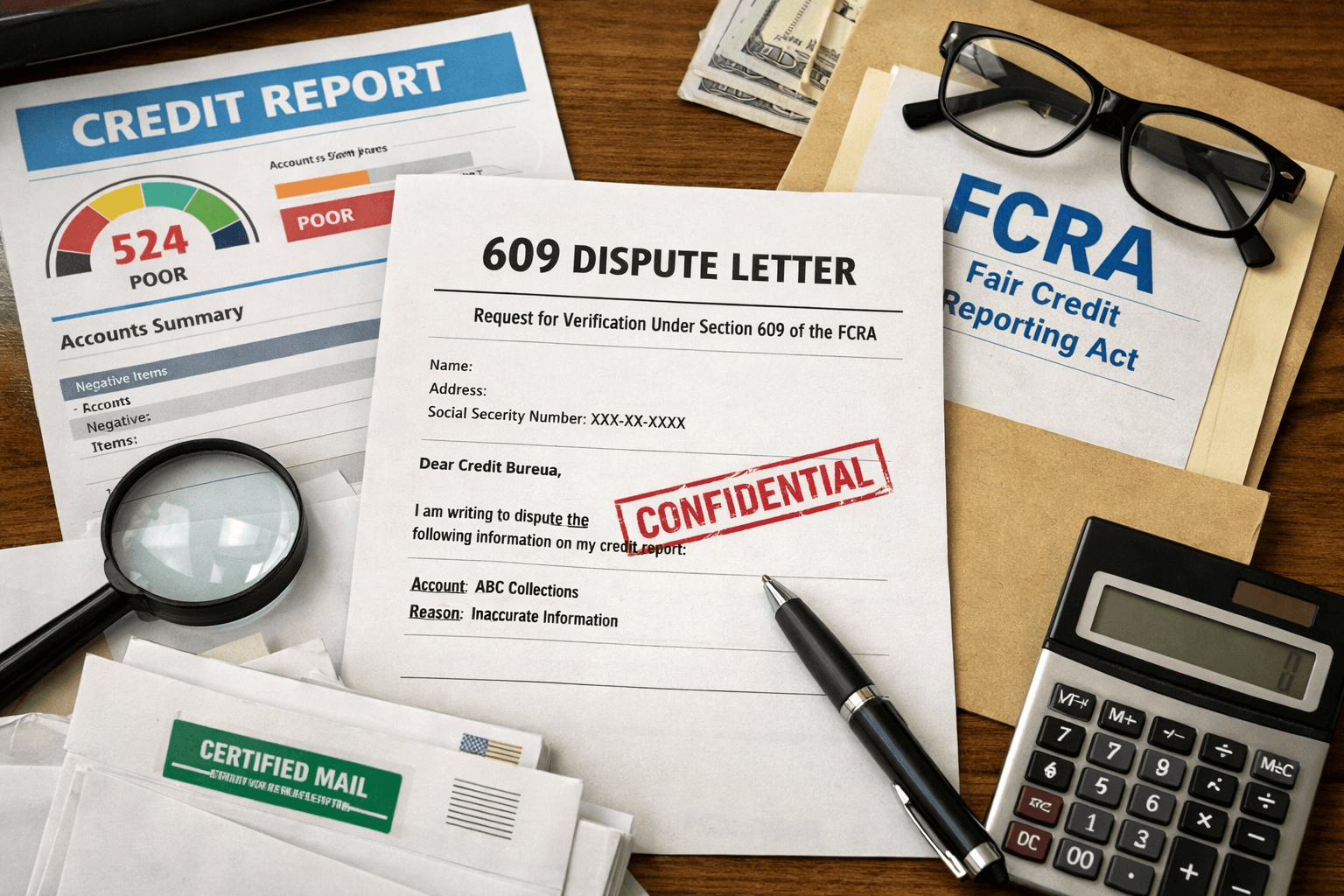

A 609 dispute letter is a formal written request to credit bureaus demanding they verify the accuracy of information on your credit report. The name comes from Section 609 of the Fair Credit Reporting Act, which outlines your legal right to request verification of any item appearing on your credit report.

"Upon request, and subject to 610(a)(1), a consumer reporting agency shall clearly and accurately disclose to the consumer... all information in the consumer's file at the time of the request." — Section 609(a)(1) of the FCRA

This is one of the most important consumer protection laws in the United States, and understanding how to use it can be a game-changer for your financial health.

Why 609 Letters Are So Effective

Credit bureaus are required by law to maintain accurate records. When you send a 609 dispute letter, you're essentially putting them on notice that you want proof of the debt or negative item. Here's what makes these letters powerful:

- Legal Obligation: Credit bureaus must respond within 30 days or remove the disputed item

- Verification Burden: The bureau must provide documentation proving the accuracy of the information

- Consumer Rights: If they can't verify, they must delete the item from your report

- Paper Trail: Creates documented evidence of your dispute for future reference

What Can You Dispute With a 609 Letter?

You can dispute virtually any negative item on your credit report that you believe is inaccurate, incomplete, or unverifiable. Common items include:

- Collections accounts — especially medical debt or old debts you don't recognize

- Late payment records — if you believe you made payments on time

- Charge-offs — accounts marked as uncollectible

- Bankruptcies — if inaccurately reported or past the allowed reporting period

- Hard inquiries — unauthorized credit checks on your report

- Incorrect personal information — wrong addresses, names, or employers

How to Write an Effective 609 Dispute Letter

A well-crafted 609 letter includes several key components. Here's what you need:

1. Your Personal Information

Start with your full legal name, current address, date of birth, and Social Security number (last 4 digits for security).

2. Clear Identification of Disputed Items

List each item you're disputing with specific details:

- Creditor name

- Account number

- The specific information you believe is inaccurate

- Why you believe it's incorrect

3. Your Legal Demand

Explicitly state that you're exercising your rights under Section 609 of the FCRA and request verification documentation.

4. Supporting Documentation

Include copies (never originals) of any documents that support your dispute, such as:

- Government-issued ID

- Proof of address

- Payment receipts

- Correspondence with creditors

What Happens After You Send Your Letter?

Once the credit bureau receives your 609 dispute letter, the following timeline typically applies:

- Within 5 days: The bureau must notify the creditor or furnisher of your dispute

- Within 30 days: The bureau must complete their investigation and respond to you

- Within 45 days: Extended timeline if you provide additional documentation

If the credit bureau cannot verify the disputed information, they are legally required to remove it from your credit report. This is where many consumers see significant improvements in their credit scores.

Tips for Maximum Success

To increase your chances of a successful dispute, follow these best practices:

- Send via certified mail with return receipt requested for proof of delivery

- Keep copies of everything you send

- Be specific about what you're disputing and why

- Follow up if you don't receive a response within 30 days

- Dispute with all three bureaus (Equifax, Experian, TransUnion) separately

How DisputeAI Can Help

Writing effective dispute letters can be time-consuming and confusing. That's where DisputeAI comes in. Our AI-powered platform generates professional, legally-compliant 609 dispute letters tailored to your specific situation in just minutes.

With DisputeAI, you can:

- Generate customized dispute letters instantly

- Track your disputes and responses

- Access multiple letter templates for different situations

- Get step-by-step guidance through the entire process

Don't let inaccurate information hold back your financial future. Take control of your credit report today with the power of 609 dispute letters and DisputeAI.

Topics

Written by DisputeAI Team

Our team of credit experts helps consumers understand their rights and fight back against inaccurate credit reporting using AI-powered dispute letter generation.