Having a collection account on your credit report can feel like a financial death sentence. A single collection can drop your credit score by 100 points or more, making it harder to get approved for credit cards, loans, apartments, and even jobs. But here's the good news: you can remove collections from your credit report, and this guide will show you exactly how to do it in 2026.

How Collections Hurt Your Credit Score

Before we dive into removal strategies, let's understand why collections are so damaging:

- Payment history is 35% of your score — Collections signal missed payments, the biggest factor in credit scoring

- They stay for 7 years — From the date of first delinquency, collections remain on your report

- Multiple collections compound damage — Each additional collection hurts your score further

- Newer collections hurt more — Recent collections have a bigger negative impact than older ones

The good news? The impact of collections decreases over time, and there are legitimate ways to remove them entirely.

5 Proven Methods to Remove Collections From Your Credit Report

Here are the most effective strategies to get collections removed, ranked by success rate:

1. Dispute Inaccurate Information (Highest Success Rate)

Under the Fair Credit Reporting Act (FCRA), you have the right to dispute any information on your credit report that is inaccurate, incomplete, or unverifiable. Collection accounts often contain errors that make them legally disputable:

- Wrong account balance or original creditor

- Incorrect date of first delinquency

- Account doesn't belong to you (identity theft or mixed files)

- Debt is past the 7-year reporting period

- Collection agency can't verify the debt

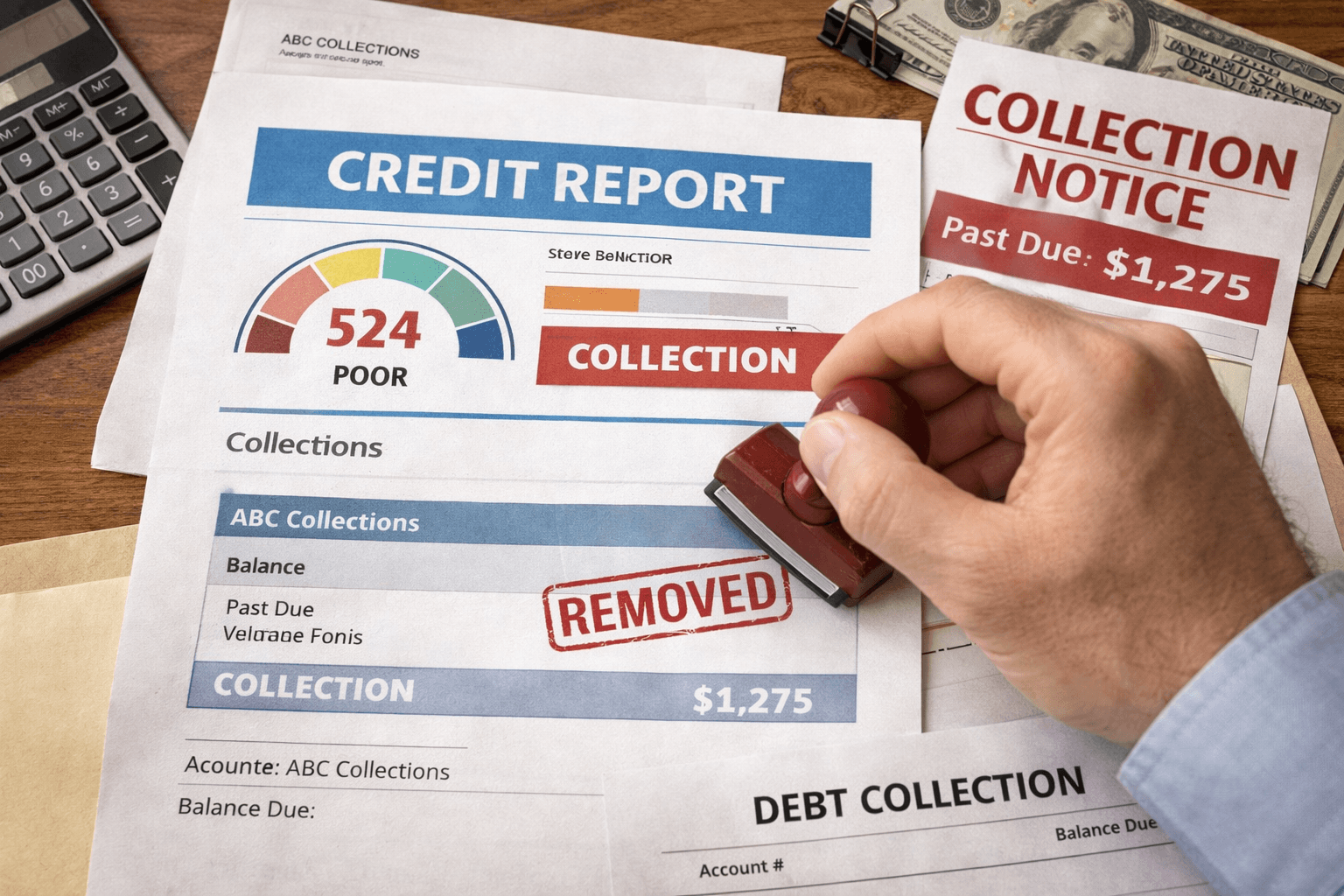

2. Pay-for-Delete Negotiation

A pay-for-delete agreement is when you negotiate with the collection agency to remove the account from your credit report in exchange for payment. Here's how to do it:

- Contact the collection agency in writing — Never negotiate by phone without documentation

- Offer to pay a portion or the full amount — Start at 25-50% of the balance

- Get the agreement in writing BEFORE paying — This is crucial

- Pay with a money order or cashier's check — Don't give them access to your bank account

- Follow up to ensure removal — Dispute if they don't honor the agreement

3. Goodwill Letters for Paid Collections

If you've already paid a collection, you can send a goodwill letter to the collection agency or original creditor requesting removal as a gesture of goodwill. This works best when:

- You have a good reason for the original delinquency (job loss, medical emergency)

- You've paid the debt in full

- You've maintained good credit habits since

- The account is with the original creditor, not a third-party collector

In your letter, be polite, take responsibility, explain your circumstances, and ask them to remove the negative mark as a courtesy. While not guaranteed, many creditors will honor these requests to maintain customer relationships.

4. Wait for Newer FICO Score Models

Good news if your collection has been paid: FICO 9 and FICO 10 score models ignore paid collection accounts entirely. VantageScore 3.0 and 4.0 also exclude paid collections. While not all lenders use these newer models yet, adoption is growing. In the meantime:

- Paying off collections still helps with manual underwriting

- Some mortgage lenders now use FICO 10

- Paid collections look better than unpaid ones regardless of scoring model

5. Wait for the 7-Year Clock to Expire

If other methods don't work, remember that collections must be removed after 7 years from the date of first delinquency (when you first missed a payment on the original account). Key points:

- The clock starts from the original delinquency date, NOT when it went to collections

- Paying or acknowledging the debt does NOT restart the 7-year clock for credit reporting

- You can dispute if the collection remains past 7 years

How to Dispute Collections With Credit Bureaus

Ready to dispute? Here's a step-by-step process:

Step 1: Get Your Credit Reports

Visit AnnualCreditReport.com to get free reports from all three bureaus: Equifax, Experian, and TransUnion.

Step 2: Identify Errors in the Collection Listing

Look for any inaccuracy, no matter how small:

- Wrong balance, dates, or account numbers

- Missing or incorrect creditor information

- Accounts older than 7 years from first delinquency

- Duplicate listings of the same debt

Step 3: Send a Dispute Letter to Each Bureau

Write a formal dispute letter citing the specific error and requesting removal or correction. Include:

- Your full name, address, and SSN (last 4 digits)

- The account you're disputing with account numbers

- The specific reason for your dispute

- Supporting documentation (if available)

- A request for investigation and removal

Step 4: Send via Certified Mail

Always send disputes via certified mail with return receipt requested. This creates a paper trail proving the bureau received your dispute.

Step 5: Wait for Investigation Results

Credit bureaus have 30 days to investigate (45 days if you send additional information). They must:

- Contact the collection agency to verify the information

- Remove items they cannot verify

- Send you results in writing

Medical Collections: Special Rules in 2026

Medical debt has different rules that benefit consumers:

- 1-year waiting period — Medical collections can't appear on your report until 1 year after the original bill

- Paid medical debt is removed — Once paid, medical collections are deleted from all three bureaus

- Collections under $500 excluded — Small medical debts no longer appear on credit reports

If you have medical collections, verify they comply with these newer rules. If not, dispute them.

How Long Does It Take to Remove Collections?

Timeline varies by method:

- Credit bureau disputes: 30-45 days

- Pay-for-delete: 30-60 days after payment

- Goodwill letters: 2-8 weeks for response

- 7-year expiration: Automatic, but may need to dispute if not removed

What NOT to Do When Dealing With Collections

Avoid these common mistakes:

- Don't ignore collections — They won't go away and may lead to lawsuits

- Don't pay without a plan — Paying without a pay-for-delete agreement won't remove it

- Don't admit the debt is yours in writing — This can restart the statute of limitations for lawsuits

- Don't give collectors your bank info — Use money orders or cashier's checks

- Don't use credit repair companies that guarantee results — No one can guarantee removal

How DisputeAI Can Help Remove Collections

Disputing collections yourself is effective but time-consuming. Writing proper dispute letters, tracking responses, and knowing what to say requires research and organization.

DisputeAI automates the entire process:

- AI-powered dispute letter generation tailored to your specific situation

- Legally-compliant letters citing the right laws and regulations

- Track all your disputes in one dashboard

- Multiple letter templates for different strategies

- Step-by-step guidance through the entire process

Whether you're dealing with one collection or multiple negative accounts, DisputeAI helps you fight back efficiently and effectively.

Conclusion: Take Action Today

Collections don't have to ruin your credit forever. With the right strategy—whether it's disputing errors, negotiating pay-for-delete, or sending goodwill letters—you can remove collections from your credit report and start rebuilding your score.

Remember:

- Always dispute inaccurate information first

- Get pay-for-delete agreements in writing

- Be persistent—success often comes on the second or third attempt

- Track everything and keep copies of all correspondence

Your credit score is too important to ignore. Start disputing today and take back control of your financial future.

Topics

Written by DisputeAI Team

Our team of credit experts helps consumers understand their rights and fight back against inaccurate credit reporting using AI-powered dispute letter generation.